Table of ContentsWhat Is The Interest Rate On Reverse Mortgages Can Be Fun For EveryoneThe Ultimate Guide To How Much Do Mortgages CostUnknown Facts About How To Invest In MortgagesThe Ultimate Guide To What Are Swaps On MortgagesThe Basic Principles Of What Are Subprime Mortgages

With the majority of reverse home loans, you have at least three organisation days after near cancel the deal for any reason, without penalty. This is known as your right of "rescission." To cancel, you must alert the loan provider in writing. Send your letter by certified mail, and ask for a return receipt.

Keep copies of your correspondence and any enclosures. After you cancel, the lending institution has 20 days to return any cash you have actually paid for the financing. If you think a fraud, or that someone associated with the deal may be breaking the law, let the counselor, lending institution, or loan servicer know.

Whether a reverse home mortgage is ideal for you is a huge question. Think about all your alternatives. You may get approved for less costly options. The following companies have more details: 1-800-CALL-FHA (1-800-225-5342) 1-855- 411-CFPB (1-855-411-2372) 1-800-209-8085. A set rate home mortgage needs a regular monthly payment that is the exact same quantity throughout the regard to the loan. When you sign the loan papers, you concur on a rates of interest and that rate never ever alters. This is the very best kind of loan if interest rates are low when you get a mortgage.

If rates go up, so will your home mortgage http://keeganroqi564.bearsfanteamshop.com/h1-style-clear-both-id-content-section-0-how-what-is-the-interest-rate-on-mortgages-today-can-save-you-time-stress-and-money-h1 rate and month-to-month payment. If rates increase a lot, you might be in huge trouble. If rates go down, your home loan rate will drop therefore will your regular monthly payment. It is typically most safe to stick with a set rate loan to protect versus rising interest rates.

Excitement About How Many Mortgages Can I Have

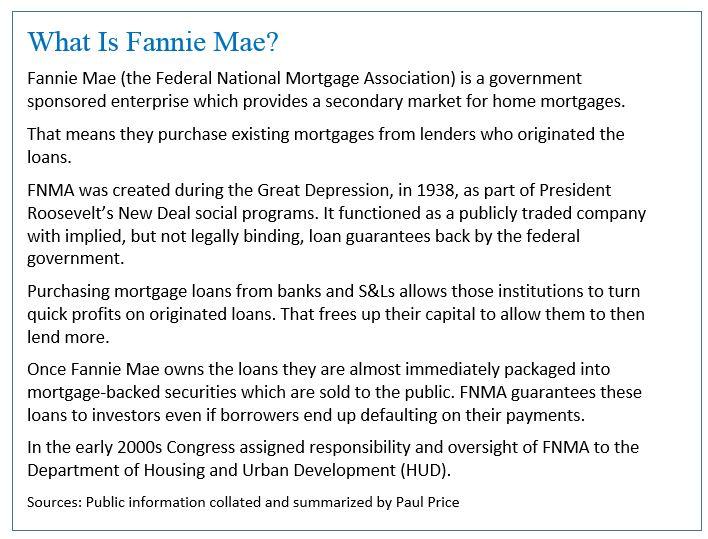

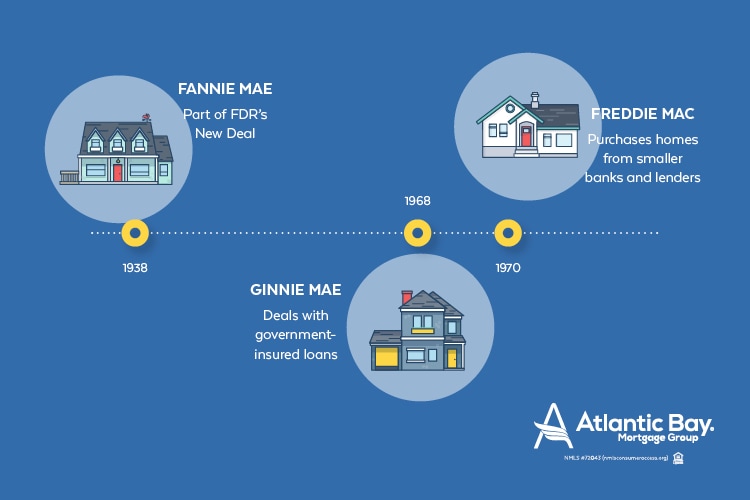

The quantity of money you borrow affects your interest rate. Mortgage sizes fall under 2 main size categories: adhering and nonconforming. Conforming loans meet the loan limit guidelines set by government-sponsored mortgage associations Fannie Mae and Freddie Mac. Non-conforming loans include those made to debtors with poor credit, high debt or recent insolvencies.

If you desire a house that's priced above your local limitation, you can still certify for a conforming loan if you have a big enough down payment to bring the loan amount down below the limitation. You can decrease the interest rate on your mortgage by paying an up-front cost, called home loan points, which consequently reduce your regular monthly payment.

In this method, buying points is said to be "buying down the rate." Points can likewise be tax-deductible if the purchase is for your primary residence. If you plan on living in your next home for at least a decade, then points might be an excellent choice for you. Paying points will cost you more than just initially paying a greater rate of interest on the loan if you plan to offer the residential or commercial property within just the next couple of years.

Your GFE also consists of a quote of the overall you can expect to pay when you close on your home. A GFE assists you compare loan deals from different lending institutions; it's not a binding agreement, so if you decide to decrease the loan, you won't have to pay any of the fees listed.

Unknown Facts About What Type Of Interest Is Calculated On Home Mortgages

The interest rate that you are estimated at the time of your home loan application can change by the time you sign your home mortgage. If you desire to avoid any surprises, you can spend for a rate lock, which dedicates the lender to giving you the initial interest rate. This warranty of a fixed rates of interest on a home loan is only possible if a loan is closed in a defined time period, normally 30 to 60 days.

Rate locks can be found in various kinds a portion of your home mortgage timeshares com quantity, a flat one-time cost, or merely a quantity figured into your interest rate. You can secure a rate when you see one you want when you initially request the loan or later on while doing so. While rate locks generally avoid your interest rate from rising, they can likewise keep it from decreasing.

A rate lock is rewarding if an unexpected increase in the interest rate will put your mortgage out of reach. If your deposit on the purchase of a house is less than 20 percent, then a loan provider may need you to pay for personal mortgage insurance, or PMI, because it is accepting a lower quantity of up-front cash towards the purchase - how much can i borrow mortgages.

The cost of PMI is based upon the size of the loan you are looking for, your deposit and your credit report. For instance, if you put down 5 percent to acquire a house, PMI may cover the extra 15 percent. If you stop paying on your loan, the PMI sets off the policy payout along with foreclosure procedures, so that the loan provider can reclaim the house and sell it in an attempt to regain the balance of what is owed.

Getting My How Many Mortgages In The Us To Work

Your PMI can also end if you reach the midpoint of your benefit for instance, if you take out a 30-year loan and you total 15 years of payments.

Put simply, a mortgage is the loan you take out to spend for a house or other piece of genuine estate. Given the high costs of buying home, nearly every home buyer requires long-lasting financing in order to purchase a home. Usually, home mortgages come with a set rate and earn money off over 15 or 30 years.

Mortgages are real estate loans that come with a specified schedule of payment, with the purchased home acting as security. In many cases, the borrower should put down between 3% and 20% of the total purchase price for your house. The remainder is provided as a loan with a fixed or variable rate of interest, depending on the type of home mortgage.

The size of the deposit might likewise impact the quantity required in closing fees and regular monthly home loan insurance coverage payments - how mortgages work. In a process called amortization, most home loan payments are split in between paying off interest and lowering the principal balance. The percentage of principal versus interest being paid monthly is determined so that primary reaches no after the final payment.

How To Compare Mortgages for Dummies

A couple of home mortgages permit interest-only payments or payments that do not even cover the complete interest. However, people who plan to own their houses must select an amortized mortgage. When you purchase a home, understanding the common kinds of home loans and how they work is just as crucial as finding the right house - what are mortgages.

In other cases, a brand-new home loan may assist you minimize payments or pay off faster by refinancing at a lower rate. The most popular mortgages provide a fixed interest rate with repayment regards to 15, 20 or thirty years. Repaired rate home loans offer the guarantee of the very same rate for the whole life of the loan, which implies that your month-to-month payment won't increase even if market rates go up after you sign.